This post has been co-authored by Niamh Barry from the FiDA Partnership, and Natasha Beale, Carson Christiano, and Alexandra Wall from the Digital Credit Observatory (DCO) at the Center for Effective Global Action (CEGA).

Credit is a powerful tool in providing liquidity: credit can smooth consumption during financial shocks, provide capital to grow businesses, ensure children’s educations, and ultimately enable people to live happier, healthier, and more prosperous lives.

Traditionally, credit providers require agent and client interaction, risk assessment uses previous financial history, loans are disbursed into a bank account, and payments are made through a bank branch. This excludes those without bank accounts, documented financial histories, or access to a branch. Since digital credit is instant, automated and remote, it could potentially overcome these barriers. Digital credit products can assess credit worthiness remotely and automatically using alternative data sources such as call records, mobile money use, and even geospatial and psychometric data, and then lend money directly to consumers’ mobile phones. Currently, the digital credit market landscape is “dominated by short-term, high interest loans made directly to consumers,” often through telco-bank partnerships.

Five years after its launch, 21.1 million Kenyans have accessed credit through Safaricom’s digital lending product M-Shwari. In addition to the telco-bank model, more and more companies are emerging to meet the growing demand for digital credit including numerous fintech companies that provide intermediary digital credit scoring services or directly originate loans to customers through app-based lending using alternative data. However, high interest rates and the volume of clients blacklisted by credit bureaus— often for late repayments or defaults on loans less than USD $2.00 —are cause for concern. Researchers and practitioners must carefully consider both the causes and effects of over-indebtedness.

What are the insights so far?

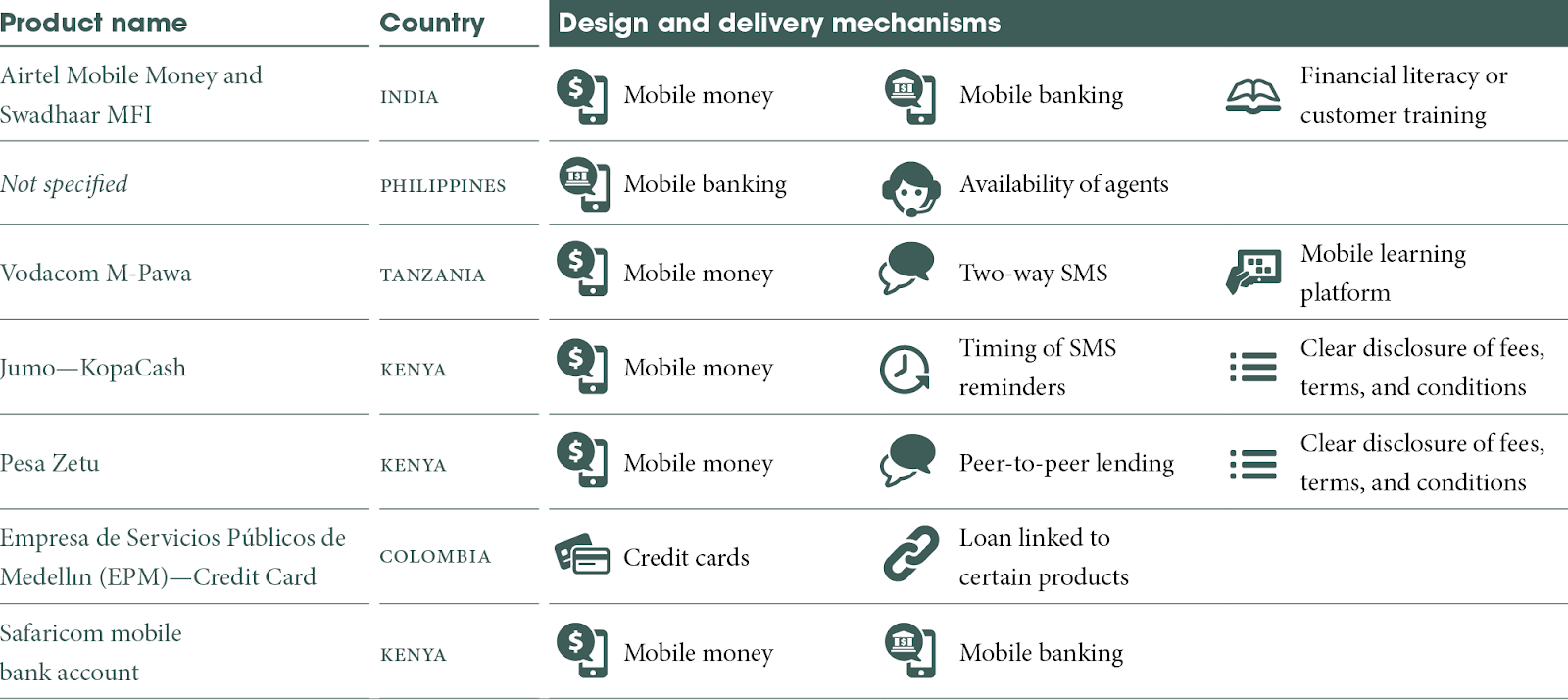

The EGM, is not confined to products that are digitised ‘end to end’, but also include credit products that have digitized some aspects of their design or delivery. Within the EGM there are just seven studies that have tested the effect of digitally enabled credit products in five countries. These studies are not yet representative of the diversity of all the digital credit products available so it is not possible to make definitive statements on the ‘impact’ of digital credit. The studies involve different markets, client groups, and design and delivery mechanisms. The table below illustrates the diversity of the digital credit products examined.

Table 1: Design and delivery of credit products

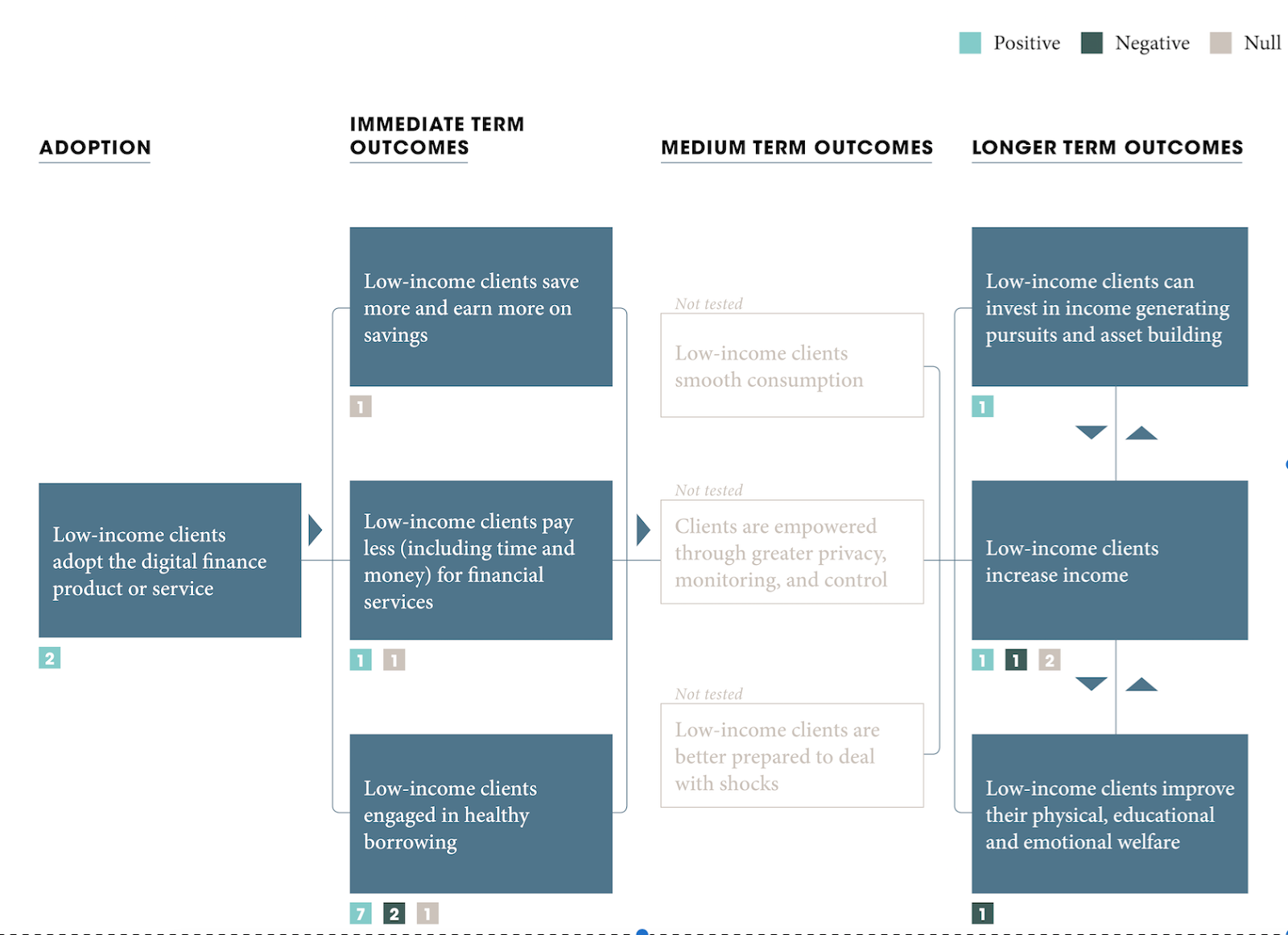

These studies include 21 tested outcomes, with ‘healthy borrowing’ being the primary outcome of focus, and just two studies providing insights on the longer-term effects. The diagram below shows the outcomes tested and the number of studies that had a positive, negative, or null effect; 57% of the credit products tested showed only positive results and 43% showed mixed results. The diversity of results is indicative of the early stage of testing and learning. As more products are tested and we continue to synthesize the evidence—with the support of investors, donors, practitioners, and researchers— clearer patterns may emerge.

Figure 1: Digital credit impact pathway

Spotlight on selected digital credit studies

We highlight just a selection of insights from an analysis of the studies within the EGM and invite digital credit practitioners, researchers, donors, and policymakers to interact with the EGM to derive insights related to their own questions.

Integrating behavioral science into repayment reminders

- CGAP partnered with Busara Center for Behavioral Economics and Jumo KopaCash—a mobile money marketplace that offers digitally delivered credit—to measure client responses to various repayment reminders. Clients were given interest-free loans via mobile money and asked to repay them after a week in order to access a larger future amount. They found that clients who received evening reminders were 8% more likely to repay their loans than those who received morning reminders. They also tested reminders that varied how they communicated the benefits of repayment. Messages either emphasized ability to access higher future loan amounts or the long-term benefits of repayment. The messages’ results varied by demographic, such as positive effects on repayment across the board for male borrowers and negative impact on repayment across the board for female borrowers.

- Also with support from CGAP and the Busara Center, Pesa Zetu— a peer-to-peer digital lender—tested the impact on repayment of content variations. One test varied the messages received by borrowers to see if different framings could improve borrowers’ on-time payments by creating a sense of social obligation to the lenders. 81% of borrowers who received reminders that included the name or number of lenders who contributed funds, were more likely to repay their loans on the day the reminder was sent, compared to only 27% in the control group.

Up front information disclosure

- The CGAP, Busara, and Jumo KopaCash experiment also tested information disclosure in a lab setting. Participants played a game in which they earned real money by completing various tasks on a computer. To buy into the game, they had to borrow money that they would pay back with what they earned from completing the tasks. Each loan outlined the different costs and repayment periods. They found that separating out the various associated costs with a loan helped reduce default rates from 29.1% to 20%. The experiment also sought to make the terms and conditions (T&Cs) more accessible by moving them up in the product menu: T&C views rose from 9.5% to 23.8% and those who viewed the content had a 7% lower delinquency rate.

Embedding interactive learning

- In another CGAP supported experiment, M-Pawa—an interest-bearing mobile money savings account that provides micro loans conditional on savings performance—partnered with Arifu, a mobile learning service, to improve savings and borrowing behaviors among smallholder farmers. Using two-way SMS on financial literacy content, researchers observed that after the interaction, Arifu users take larger loans (1,017 TZH/$0.44), repay sooner (by 5.46 days), and have larger first payments (1,730 TZH/$0.76 more) compared to their behavior before interacting with Arifu.

Limiting credit to certain products

- With the support of the IDB Group, Empresa de Servicios Públicos de Medellın (EPM)—a large retail store—created and tested the ‘Social Financing Program’ in Colombia. The program provided credit to allow EPM customers to buy various home and personal goods in establishments affiliated with the program. By using its own data to evaluate credit applications, EPM required less information than traditional banks. The initiative aimed to serve low-income borrowers with less access to formal finance by enabling them to build a credit history and buy goods. They found no effect on uptake of other financial tools (such as savings accounts and formal credit). However, the results show that the credit card was associated with an increase in the number of household goods owned, such as floors, kitchens, and bathrooms. The intervention showed mixed and limited results on self-reported well-being outcomes.

The value of being in an ecosystem with more than one financial tool

- In partnership with Safaricom, researchers piloted the use of a mobile banking account (MBA) and a locked savings account (LSA) to encourage parents to save for their children’s transition to secondary school. Use of the MBA increased the likelihood of credit access within the platform. Parents in both treatment groups were between 3% and 5% more likely to draw on an MBA loan than the control group. The treatment estimates also suggest that between 12% and 18% of users who opened an account as a result of the program took advantage of the credit option.

Detailed insights on digital borrowers in Kenya and Tanzania*

CGAP and FSD Kenya recently conducted two large-scale, nationally representative phone surveys of mobile phone owners in Kenya and Tanzania. The survey findings are numerous and a few are highlighted here.

- The primary users of digital credit products are predominantly young, urban self- or wage-employed men.

- Most borrowers use the loans to meet business and day-to-day needs. Loans are rarely used for medical needs or emergencies.

- Digital borrowers use more financial services than the average Kenyan or Tanzanian adult.

- About half of borrowers report having repaid a digital loan late, and a significant proportion report having defaulted.

- Digital credit is only one loan source among many. 33% of digital borrowers in Kenya and 25% in Tanzania were juggling loans from two or more sources (digital and nondigital) at the time of the survey.

- More than a quarter of borrowers in Tanzania and nearly a fifth in Kenya, reported experiencing poor transparency of fees or terms.

It evident that better transparency and consumer protection requirements are needed and regulators, donors, and investors alike will need to play a role in ensuring the digital credit market grows responsibly.

The takeaways

The evidence on the client impact of digital credit is limited, particularly for longer-term welfare outcomes. But insights, particularly for promoting ‘healthy borrowing,’ are surfacing:

- The framing and timing of SMS reminders can improve repayment rates and protect borrowers. But the differential effects observed between men and women suggest that further testing is needed.

- Making T&Cs more salient, accessible, and thus viewed and understood by borrowers may lead to better borrowing behavior and repayments.

- Using interactive learning content on financial literacy has shown promising results for repayment behavior.

- Being in an existing financial ecosystem may improve use of other financial services, such as using savings to access loans.

Beyond borrowing behavior, we know very little. In 2016, the Center for Effective Global Action (CEGA) at the University of California, Berkeley launched the Digital Credit Observatory (DCO), funded by the Bill & Melinda Gates Foundation, to call attention to open research questions around digital credit. The DCO noted —in 2016—that, to their knowledge, “not a single quantitative impact evaluation has rigorously measured the social and economic impacts of digital credit.” This is in contrast to the 90 (quantitative) studies included in a more recent meta-analysis of traditional microcredit. Only very recently has a FSD Kenya supported study provides insights on the longer term effects of a Kenyan digital credit product.

In order to advance the discourse on digital credit, the DCO manages a set of coordinated studies answering key questions related to the impacts of digital credit in emerging markets, as well as the effectiveness of promising approaches to maximizing benefits and minimizing risks to low-income consumers. The research portfolio also considers the heterogeneity of effects of products and their design and delivery on different client segments. Such insights from the DCO are possible due to engaged donors, practitioners and researchers. The digital credit community must continue to look for opportunities to gather impact insights so we keep learning how to best move forward in the journey toward meaningful financial inclusion.

*While this study was concluded after the literature review period ended and thus will be included in the next iteration, the findings provide the most current and detailed nationally representative evidence available on digital credit and related consumer issues for users in East Africa.

FiDA is publishing a series on insights derived from an analysis of the latest Digital Finance Evidence Gap Map (EGM) update. This is the third blog, others will include impact insights on payments and transfers, the design and delivery of various products, and where (people and location) we have been looking for impacts. Previous posts:

The studies in the EGM, represent our best knowledge of digital finance impact insights. New studies are ever emerging and thus the EGM will continue to evolve. If you have questions on the EGM, are interested in discussing research priorities, or know of relevant digital finance impact studies that meet the inclusion criteria, please contact ideas@financedigitalafrica.org.